This academic year has brought changes to fiscal management across colleges, departments, and other units. One of these changes is a recently implemented tax on carry forward accounts. A carry forward account is any account that “carries forward” a balance from the previous fiscal year into the current fiscal year. The source of funds in such funds can come from different sources, including start-up packages, accrued salary savings from effort applied to extramural grants, and F&A revenue. The Faculty Senate Executive committee has asked for clarification concerning how the tax on carry forward will be calculated and how the tax will be administered. Here is what we have learned.

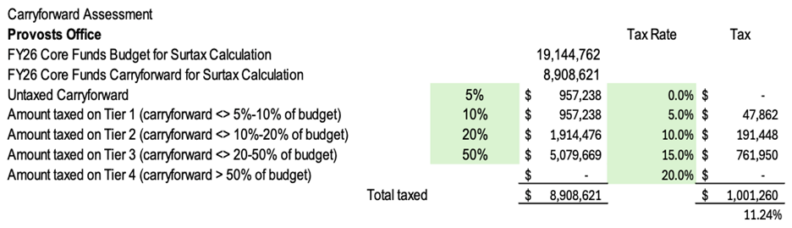

The tax on carry forward is calculated at the level of the college or campus. It is a tax on the aggregate total of all individual carry forward accounts in the unit. In the current fiscal year (FY26), the tax on carry forward surtax is calculated using a progressive method (much like federal income tax), and based on the unit’s carry-forward balance as a percentage of the unit’s FY26 base budget allocation. The first 5% of carry forward is fully exempt from the tax. Amounts above 5% of total base budget are taxed incrementally, with higher surtax rates applied to the portion of carry forward that falls within each tier. The percentage tax rates for FY26 are shown in the following table (courtesy of Matt Skinner, Vice President for Finance and Business Services).

| FY26 Tier | FY26 Carryforward Range (as % of base budget) | FY26 Surtax Rate |

| Exempt | 0–5% | 0% |

| Tier 1 | 5–10% | 5% |

| Tier 2 | 10–20% | 10% |

| Tier 3 | 20–50% | 15% |

| Tier 4 | Over 50% | 20% |

For FY26, the percent calculation of Carry Forward Range (middle column) is based on carry forward in General Fund (FD001) and Administrative Fees and Interest (FD080) accounts. The calculation for FY26 excluded F&A funds (FD076). Below is an example of the tax calculation given by Leslie Brunelli, Executive Vice President for Finance and Operations, taken from her presentation to the Faculty Senate in October of 2025.

The surtax is new and the methodology for calculation of the tax may change in future years. The FY27 tax method will be determined as part of budget planning process this spring (March-June).

The tax rate process described above is applied at the level of the colleges and campuses. How these individual units tax the various individual accounts is up to the leadership of these units. It is not required that units apply the university tax rate evenly across all their accounts. For instance, colleges and campuses could choose to exempt certain types of accounts from taxation and tax other accounts at a higher rate, so long as the total tax on the unit is met.

Comments